The media landscape doesn’t evolve on a predictable timeline. Platform innovation, shifting consumption habits, and new buying mechanics move at a speed where if you blink, you probably missed it. For brands, keeping pace isn’t just about awareness, it’s about knowing where to lean in, when to pivot, and how to extract real value from change.

At Ocean Media, we track these shifts with precision, evaluating every development through the lens of performance, efficiency, and audience behavior. Our focus isn’t on reacting to trends, but on understanding how they reshape planning, activation, and measurement, as well as where they create opportunity for smarter media investment.

In this year’s trends piece, we examine five key areas shaping the future of media buying in 2026 and beyond. While these are predictions, they reflect clear signals emerging across the industry today. Together, they outline where media is headed next and how brands can position themselves ahead of it.

Social Platforms Will Extend Their Audiences Into CTV

Social platforms have mastered one thing better than anyone else: audience intelligence. Their ability to understand interests, intent, and behaviors at a one-to-one level is unmatched. What they haven’t historically controlled is premium, full-screen television inventory.

That gap appears to be closing.

Recent industry conversations point to growing interest from social platforms, Meta included, in how CTV buying actually works in practice. Questions around deal structures, optimization, and measurement suggest that these platforms are actively evaluating how CTV fits into their broader ecosystems. Rather than focusing solely on content ownership, the momentum appears to be shifting towards exploring ways social audience signals could be extended into CTV environments over time.

Pinterest’s acquisition of tvScientific further confirms this trajectory. At the same time, Instagram is bringing Reels to Amazon Fire TV to compete with YouTube. Social platforms are watching Amazon, Google, Netflix, and The Trade Desk capture outsized growth from CTV, and they don’t want to remain sidelined. Acquiring CTV-native buying infrastructure allows social platforms to shortcut years of development and immediately plug their audience graphs into television inventory.

The appeal for advertisers is obvious. Brands heavily invested in social, particularly DTC and mid-market advertisers, could soon activate CTV by simply extending existing campaigns. The promise is simplicity: one platform, one audience definition, unified reporting, and deduplicated reach across screens. CTV has also proven its worth on several fronts for brands seeking to maximize the value of their ad buy, particularly when the choice is between CTV and linear.

However, this approach is not without tradeoffs. Social platforms do not own the inventory, which means pricing may be less efficient than buying directly from publishers. More importantly, CTV is a shared household environment, not a one-to-one experience like mobile feeds. The precision that makes social so powerful may soften when applied to a living-room screen.

Why it matters for your brand:

This trend signals a shift toward audience-first planning at scale. Social platforms aren’t trying to replace CTV buying, they’re trying to make it accessible to advertisers who have historically avoided it. For some brands, this will be an on-ramp to television. For others, especially larger advertisers, it reinforces the need for expert guidance to balance simplicity against control, cost, and accuracy.

– Kevin Telkamp, Ocean Media, VP, Media Operations

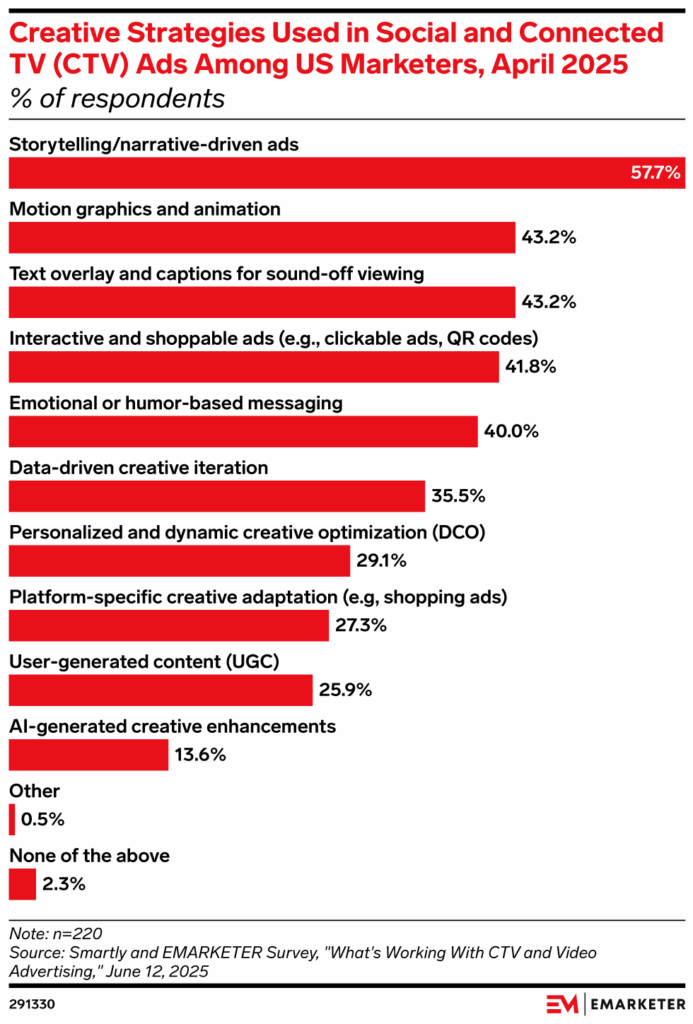

Interactive and Shoppable Ads Become Standard Across Screens

By 2026, interactive and shoppable ad formats will no longer be viewed as experimental or “nice-to-have.” They will become a standard placement option across social, linear, and CTV, driven by evolving viewer expectations and platform investment in commerce-enabled media.

What began in social such as tap-to-shop, product tags, in-feed checkout, etc., has set a clear precedent for how consumers want to engage with advertising. That expectation is now migrating to the largest screen in the home. As CTV platforms mature, interactivity is shifting from novelty to necessity, giving brands the ability to move viewers from passive awareness to active engagement without leaving the viewing environment.

Interactive ad formats consistently drive stronger engagement, longer time spent, and clearer intent signals than standard video placements, especially in environments where attention is harder to earn. Marketers have taken notice, as they have increasingly incorporated the ad capabilities to its strategy arsenal.

Social platforms have already proven the model. According to Horowitz Research, nearly 45% of U.S. consumers report making a purchase directly through social platforms, reinforcing that commerce-enabled media is now mainstream behavior, not fringe adoption. As CTV platforms introduce more seamless interaction mechanisms such as QR codes, mobile handoffs, and remote-enabled prompts, engagement on the largest screen in the home continues to rise.

Industry benchmarks show steady growth in CTV engagement metrics as interactive formats become more prevalent, indicating increasing viewer comfort and willingness to act rather than simply watch. Platform investment in these formats suggests interactivity is being built for scale, not experimentation.

The biggest challenge facing interactive and shoppable media today is fragmentation.

Each platform offers its own version of interactivity, with different creative requirements, user experiences, and measurement approaches. While some interactive formats are beginning to flow through programmatic pipes, many still require direct integrations, custom executions, or platform-specific buys. Attribution is equally inconsistent, ranging from engagement-based metrics to site visitation, lift studies, or downstream conversions.

This fragmentation creates friction for brands trying to scale but also presents an opportunity.

Advertisers that move early can test formats, identify what truly drives impact, and establish benchmarks before interactive placements become standardized and more competitive. With the right strategy, brands can streamline executions across platforms, align on consistent measurement frameworks, and avoid treating interactivity as a one-off tactic rather than a scalable capability.

Why it matters for your brand:

As media continues to evolve toward addressability and commerce, the distinction between brand and performance advertising is fading. Interactive and shoppable formats sit directly at that intersection of turning high-attention environments like CTV into actionable moments rather than passive impressions.

By 2026, interactivity won’t be a differentiator, it will be an expectation. Brands that have already tested and refined their approach will be better positioned to drive measurable outcomes across screens, while those that wait risk playing catch-up in a more crowded and less forgiving marketplace.

– Stephanie Stanczak, Ocean Media VP, Media Investments

Decisioned PMPs Are Becoming More Cost-Effective Than Direct IO, For Now

For years, the hierarchy was clear: Direct IO meant guaranteed inventory and premium pricing, while programmatic offered flexibility with less certainty. That model is starting to flip.

In the second half of 2025, Netflix and Spotify, two of the most powerful publishers in video and audio, began pricing decisioned PMP inventory at floor rates meaningfully lower than their Direct IO or Programmatic Guaranteed deals. This shift isn’t driven by a lack of demand, but rather by operational efficiency.

Direct IOs require publishers to dedicate internal resources to campaign setup, pacing, optimization, and reporting. PMPs reduce that burden significantly. By pushing more spend into programmatic pipes, these publishers lower overhead, even if it means giving up guaranteed revenue in the short term.

For advertisers, the appeal is immediate: lower entry CPM’s, better programmatic signals and transparency, and flexibility to optimize or pull spend if performance lags.

However, this isn’t a purely altruistic move.

PMPs are dynamic; while floors may start low, there is no ceiling. As more buyers compete for the same premium inventory, clearing prices can quietly rise. What begins as a cost advantage can gradually inflate without the visibility or negotiation checkpoints that come with Direct IOs. The long game is prioritize efficiency now, and allow auction pressure to drive pricing later.

Why it matters for your brand:

This trend fundamentally changes how premium inventory is accessed. PMPs are becoming the preferred pathway for publishers and a powerful lever for buyers, but they require vigilance. Advertisers must continuously benchmark PMP pricing against IOs, monitor floor creep, and understand when flexibility outweighs guarantees.

More broadly, this underscores a critical shift: inventory procurement is no longer black and white. It’s a spectrum of options, each with tradeoffs. As blue-chip publishers lean further into programmatic, the role of a trusted agency becomes even more essential to navigate these shades of gray and ensure efficiency today doesn’t become inflated cost tomorrow.

– Kevin Telkamp, Ocean Media, VP, Media Operations

First-Party Data Becomes Table Stakes for Streaming TV

As streaming continues to take a larger share of video budgets, relying on broad demos or platform-only targeting will get harder to justify. As third-party data signals weaken, CTV partners are putting more emphasis on authenticated identity, which is pushing first-party data to the center of streaming activation. Advertisers who can’t bring their own data into these environments will feel the gap quickly, both in cost and performance. However, more brands are prioritizing strategies and efforts toward the importance of first-party data.

From a strategy standpoint, this shift fundamentally changes how CTV should be planned. Streaming TV is no longer just an awareness channel or a one-to-one replacement for linear. When powered by first-party data, CTV becomes a precision layer within the video mix, enabling brands to reach higher-value and priority audiences, control exposure through smarter suppression, and create more intentional sequencing across video, social, and performance channels.

As this evolution accelerates, the biggest challenges in 2026 will not be about access to inventory or media buying mechanics. Instead, they will center on execution. Many brands are still working through data readiness, internal ownership, and alignment across teams, all while navigating increasingly strict privacy and consent requirements that govern how customer data can be activated in streaming environments.

At the same time, operational complexity will continue to rise as clean rooms, identity frameworks, and publisher-specific data environments become standard. Limited interoperability across platforms means advertisers must be more deliberate about how data is structured, activated, and measured.

Why it matters for your brand:

The brands that win in 2026 will be the ones that invest early in scalable, privacy-safe data foundations and treat CTV as a core activation layer. First-party data won’t just improve targeting. It’ll unlock efficiency, flexibility, and long-term advantage in a premium streaming landscape.

– Katie Harker, Ocean Media VP, Digital Strategy

NFL Will Renegotiate Broadcast Rights Early

The NFL is likely to push for an early reconsideration of its broadcast rights, ahead of the official 2029–2030 opt-out window, with the consent of its current partners. An early renegotiation would almost certainly reshape the current landscape, with at least one legacy broadcaster losing share or being left with a smaller package, while a major streaming platform picks up a significantly larger portion of NFL inventory. As streaming viewership continues to scale, the league has little incentive to wait.

Early results from streaming-led NFL packages continue to strengthen the league’s leverage. Amazon has seen consistent year-over-year growth since acquiring Thursday Night Football, with the most recent season opener drawing over 17 million viewers; its largest audience to date and roughly 10% higher than FOX’s previous peak during its final season of TNF. YouTube’s 2025 Brazil Game surpassed 18 million viewers, reinforcing the global and scalable reach streamers can deliver.

With platforms like Amazon, YouTube, and Netflix aggressively competing for premium live content, the NFL is uniquely positioned to command higher long-term value by expanding marquee moments and testing new distribution models.

For consumers, continued fragmentation of live sports rights creates growing complexity, forcing fans to follow their favorite teams across multiple platforms and subscriptions. For advertisers, however, this fragmentation also creates opportunity. Bundled access, such as ESPN Unlimited/ FOX One, offers pathways to strike consolidated deals with fewer partners while still reaching audiences across multiple environments. As streamers and broadcasters look to differentiate their NFL offerings, advertisers may find more flexible packaging, enhanced data access, and cross-platform activation opportunities than traditional broadcast deals historically allowed.

Why it matters for your brand:

The NFL remains the most powerful property in live sports, and its next rights shift will set the tone for the broader sports media ecosystem. Brands that understand how to navigate a streamer-heavy NFL landscape, such as balancing reach, data, and flexibility, will be better positioned to capitalize on premium live moments as rights continue to evolve. As broadcasters and streamers compete more aggressively, the advantage will shift toward advertisers who are prepared to adapt alongside the league.

– Kevin Cozine, Ocean Media, Senior Director, Media Investment

To learn more about advertising trends, brand strategy, and media investment, please contact us!